I’m challenging myself to reach a bare bones level of wealth needed for me to retire early within the next three years. Naturally that has me considering the nature of wealth, security, and money. With regards to money I tend to fall into two different mental habits, neither of which really serve me fully. The first is to focus on increasing my income. I realized the other day this is almost completely irrelevant on its own. The other habit of mine is to focus on cutting expenses. Again this is almost as irrelevant as increasing income. Reducing expenses does tend to reduce consumption of energy and resources, thus reducing my ecological footprint, but with regards to wealth and security unless I can sustainably reduce it to zero this too is completely irrelevant on its own.

(Please note some of the links in this blog post are affiliate links. What this means is that should you click through them and make a qualifying purchase I will receive a commission which I’d certainly appreciate since it helps support this blog project. However, this shouldn’t increase your cost any, and certainly don’t ever feel like I’m pressuring you to buy things through the links I offer or anywhere else. I’m all about being frugal first!)

That making more money or spending less of it are irrelevant to wealth creation probably sounds a bit absurd. Let me explain this further, along with the realization I had. If I was making a million dollars a day but spending a million and one I would be broke. Likewise, if I reduced my expenses to a mere dollar a day, but could only bring in fifty cents I would be just as broke. It makes no difference either way.

The realization was just bringing into greater awareness something I already knew. Wealth and security comes from the relationship between income and expenses. It’s all about the gap between them! That is what matters and where the magic happens.

It probably seems like I’m splitting hairs here since obviously to increase the gap between income and expenses one can either focus on increasing the amount of money made or reduce the cost of living. However, by not focusing attention directly on the relationship between the two funny things can happen.

My tendency in life has usually been to focus on frugal, simple living, keeping my monetary needs low. This has been a great strategy for allowing me to launch myself as a fully self employed artist, a career path not known for those seeking easy high levels of income. Once I established myself full-time I was able to develop my art business more quickly and build greater income levels since I could devote most of my time to it, rather than spending my days working a “normal” job for money.

The catch here though is that when I’m focused so hard on keeping expenses low I tend to get into a poverty mindset, seeing every dollar as precious, as though I might not be able to keep an ample supply coming in. I start to identify as someone who can’t make much money, and by some weird quirk of the universe this is exactly what I start to manifest. I suspect this is mostly because my mind stops looking for and recognizing opportunities for greater income. There is certainly less urgency to do so. I see this even now during this past year as I’ve refocused on frugal living, seeking to get my normal non-business expenses below $500 a month. When I become capable of living on less I seem to find myself making less.

I’ve spent many years seeking to overcome my inherent tendency to believe I can’t make a high income and must be frugal. During this time I really focused on increasing income and building my business. I was reasonably successful with this, but result was that as I made more I also spent more. When having a higher flow of money coming in it just became easier to spend and extra $20, or $100, or $1000 here and there. As long as I had more coming in than going out it didn’t seem to matter much. I was still building up my savings right?

Thankfully my careful tracking of all money coming in and going out allowed me to see that I wasn’t spending more than I made. Surely I wouldn’t let such a thing happen… and then it did. Income as an artist can be quite sporadic with huge swings up and down. So it’s not uncommon to lose money one month only to have a large gain another. I thought I was keeping all this in check and then one year when doing the final annual tally I was utterly shocked to see I’d spent more than I made! I can’t even say it was an abnormally bad year for income. It wasn’t. Here I thought I was Mr. Financial Savvy and I went and allowed that to happen. I was focused so much on increasing my income, which was flowing in nicely, that it became easy to spend even more.

Thus I see these as the hazards of directing my attention to either reducing spending or increasing income. My realization was that I’ve never really focused on the gap in between, the rate of savings. Admittedly it’s a bit harder to focus on this because the data points aren’t as readily apparent. They have to be extrapolated from the other figures, putting the income and expenses into context with each other over a period of time. However, I think this is the way I need to go. Where I focus my attention is what seems to naturally grow, and it is the saving rate that I want to grow if I am to meet my early retirement goal. So I’m going to be adding a new figure in my monthly tabulations, one that shows the gap. Hopefully that gap will always be on the plus side, thus being a savings rate, rather than the negative side indicating more spending than income.

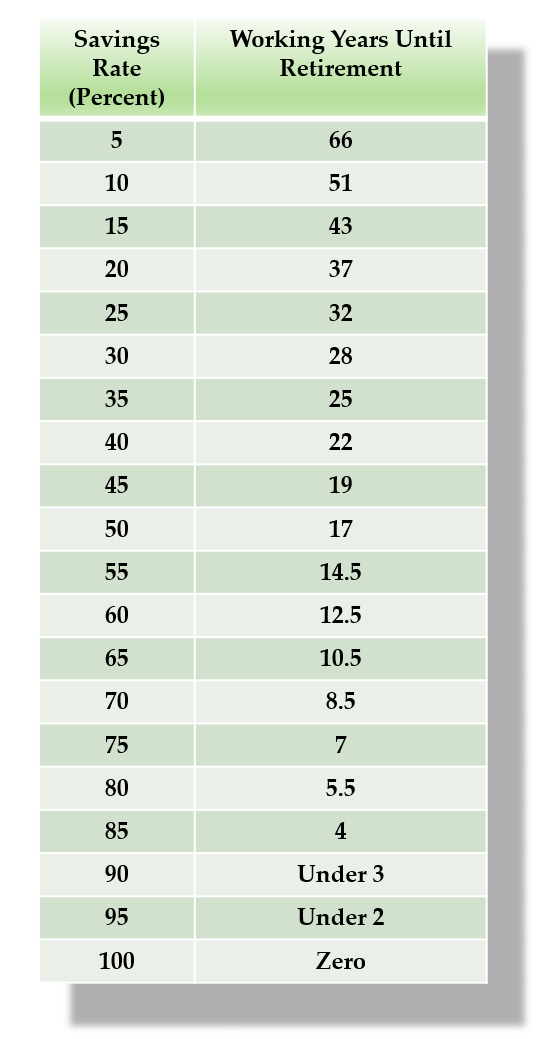

I suspect staying focused on the gap will also help eliminate the potential problem of always seeking more no matter how much I have. It should help make clear when “enough” is reached. This is because if you graph out your gap between spending and earning with the number of years needed to retire at each level of savings what you get is an exponential function, the sort of hockey stick like graphical line. At this point I feel I need to direct you to a blog post by Mr. Money Mustache called “The Shockingly Simple Math Behind Early Retirement” where he really lays this all out. He is generally considered one of the modern day gurus of the Financial Independence/ Retire Early (FIRE) movement and I can highly recommend his blog if you are at all interested in this sort of thing.

Based on the chart he provides you can see that saving just 5% of your annual income would put you on track to retire in 66 years based on his investment assumptions. If that was boosted to 10% then 15 years get shaved off that number bringing it to 51! However, if you were at a 90% saving rate and increased it to 95% then you are only cutting off a about a year. At 95% though you could retire in less than 2 years!

{kind=link}

So if I’m paying attention to my saving rate rather than my income level what happens as income gets so far ahead of my expenses is that it becomes stupidly obvious when I have enough to support my lifestyle because at a high enough savings rate all the effort to get a bit higher will only have marginal effects on time to retirement. Put another way this should reveal to me when making more money isn’t really generating substantial gains in security. Rather it is just consuming more of the hours of my life I can’t ever get back. My goal is not to make the most money. It is to get the most satisfaction and fulfillment out of life. This might coincide with activities that generate income (I do enjoy my work life as an artist after all) however, it might not too. What sort of art might I do if I had no concerns about ever selling it?

I guess ultimately my goal here is to get the money portion of my life taken care of so I can focus on anything and everything else. If I can’t clearly identify when I’ve reached the “enough” stage though I’m likely to get stuck trying to always earn more, never feeling secure.

My savings rate last year was 65%, which by the Mr. Money Mustache chart would put me at 10.5 years to retirement if I was starting from zero. Fortunately I’m not starting there! I already have almost 30 years of savings which at one point seemed good. Now though I have to wish I had learned to mind the gap SO much sooner. If I had I could have been financially independent for decades now!

I should also note that in “The Shockingly Simple Math Behind Early Retirement” blog post, he points out that reducing expenses is a more powerful strategy than increasing income. The less you can comfortably live on the more you have to invest and the less you’ll need from those investments. To this I’ll add that the relationship of the 3 E’s (economy, energy, and environment) indicates that you’ll likely also be using less fossil fuels and putting less of a strain on all environmental resources. Those are goals I’m after in addition to establishing a more secure personal economy.

In this post thus far I’ve pretty much just focused on financial capital, and I will admit when I think about wealth this is where my mind normally goes first and foremost. However, a book I’ve found enlightening called “Prosper!” by Chris Martenson and Adam Taggart lays out the idea of 8 forms of capital, of which financial capital is only one. The others are living capital, material capital, knowledge capital, emotional capital, social capital, cultural capital, and time capital.

When this thought of focusing on the gap came to me I started thinking how this might apply to some of the other forms of capital. Does the idea that wealth and security lies in the space between what you bring in or generate, and what you consume fit any of these others? I feel a bit fuzzy on some of them, but it seems to apply clearly to others.

Living capital for example could be seen as a couple different things. The health of an ecosystem would be living capital. If we are consuming the resources of that ecosystem faster than they can regenerate we would be far less secure and wealthy than if we stayed below the rate of regeneration. With topsoil for instance there are ways to grow food that actually increases the creation of new topsoil in the process. This would clearly boost wealth over normal agricultural practices that deplete topsoil.

Another form of living capital would be the health of our bodies. If I wanted to increase the gap between what I generate and what I consume here I would be engaging in practices that make my body healthier and stronger at a greater rate than I do things that harm and hinder my body. The greater the gap the greater my health!

Material capital would be manufacturing or acquiring material goods at a faster rate than I consumed them. I’m suspicious of the idea that a huge gap here would always be a good thing. Thoughts of hoarders comes to mind. Perhaps the check on this one is that most material goods come with their own maintenance requirements such that they involve a drain of other capital just to have. So material capital that isn’t being utilized functions as a steady drain of resources. I probably need to spend more time ruminating on this one.

With knowledge capital would the gap be knowing more than you need? Whereas having no gap would be not knowing what you need to know? The larger your gap the more prepared you are for what life offers, or throws at you? I’m not sure on this one either.

I suspect emotional capital would be similar to knowledge capital in that the gap would be having greater emotional strength and capacity than the demands life throws at you.

Social capital would clearly be having greater, stronger, and deeper social relations than your need to draw upon them. Thus helping to ensure that when you did have a need someone would be there to assist.

Cultural capital always feels like a funny one to me since there is not much one can do about it. If there isn’t a gap between our culture’s ability to handle situations and the demands placed upon it we get cultural collapse, which wouldn’t be a pretty thing.

Finally, there is time capital. Ultimately the gap here is between the time you are born and the time you will die. It’s a form of capital that is constantly being consumed. Religious or spiritual beliefs might factor into how one sees this. I’d like to think that by paying attention to the living capital of my body and my emotional (spiritual) capital I have the ability to increase the gap between birth and death. Still it seems fixed within a certain range.

A good portion of the impetus to achieve financial independence/early retirement is the recognition that my time capital is steadily draining away. I don’t want to be required to work, trading my time for money my whole life. I’d like to have the freedom to direct my life to other pursuits if I so chose. It’s easy for me to get into routines, just coasting through life. To be honest I take a fair amount of comfort from routines. What I need to keep reminding myself of though is to mind the gap! With time capital it is constantly being whittled away. Here especially the gap is where the magic happens! I need to stay focused on it and seize the opportunity to live in this time, this place, and this body to the best of my ability!

So one of my new goals is to Mind the Gap as a means to building security and allowing me to sculpt my life through a wider range of opportunities once I can be freed from the need to pursue money.

Studio Snippet

As I write this in late June of 2019 I’ve got a workshop coming up soon at the Creative Side Academy in Austin, TX. It will be focused on chasing on a vessel form. For these workshops I bring a very basic set of chasing tools for each student to use in class which they can purchase and keep afterward if they wish.

This means that in preparation for the workshop I’ve got a lot of chasing tools to make, and thus this is what’s been happening in the studio this week.

I’ve also recently gotten a bunch of new tools to try out in an effort to make the whole process more efficient. Though this also means there has been a certain level of inefficiency in the process of this batch as I try different things to find what’s best.

One tool that has clearly stood out as superior for the major grinding and shaping work is a 4.5″ grinder with a 40 grit flap wheel. I’ve done this before with my 6″ wide belt sander. That works, but takes a while. I had the good fortune to be able to use some seriously major industrial belt sanders on this batch of chasing tools, thinking at least one of them would be superior for the job. The one that worked best was an absolute monster of a machine! If I could even afford one it wouldn’t fit in my studio, never mind the power requirements. It worked well, but to my shock the flap wheel on the grinder worked way better! I’ll note too that the flap wheel worked better than a grinding wheel for rapid removal of material!

I’m happy to have a site where I can again allow comments. (I had to shut them off on my main website because the spam was simply uncontrollable!) So please I encourage you to share thoughts of your own. My general rule about comments though is just to play nice. Differing views are fine, but I’m not interested in engaging in or moderating verbal fights. If I feel things get out of hand, by whatever criteria I decide, I’ll just start blocking or deleting things.

Thanks for this post, David. You gave me lots to think about!

You’re welcome Cara. I suppose I did pack a lot of different concepts into this one, esp. when adding in the 8 forms of capital.

As one who has already retired I can speak from experience Make sure you will be happier retired. I have been retired for five years now & have still not found what made me as happy a My lifes work did.

As one who has already retired I can speak from experience Make sure you will be happier retired. I have been retired for five years now & have still not found what made me as happy a My lifes work did.

Thanks for the word of caution Larry.

To me the beauty of this system is that you don’t have to retire if you don’t want to. It just becomes and option always available should you decide to take a different path in life. It is certainly true that many people find their purpose and passion in life through their jobs. In my case I doubt that I’ll actually quit my job as a self employed artist. I love what I do! However, if financial need for employment was taken out of the picture even more opportunities open up whether that taking a day or two off to read a good book, going out hiking for a week or two, or engaging in art projects that I’m passionate about but aren’t very marketable (I definitely got some ideas here).

I hope you can find that greater happiness in retirement, or perhaps pursue the option of returning to employment in your life’s work on your own terms.

Well, you gave some food for thought with this remarkable post. Kept me “chewing” while I did chores in the garden yesterday. I’ve always had an attitude of enough towards money. However my situation was (and there were some pretty bad times) I always had enough to feed and dress me without looking poor. I’m frugal by nature and don’t mind secondhand & don’t shy away from repairing something :-). But when I want something, I want the best for what money can buy and I will research the best options. An example comes to mind: In the early days of computers, I decided I wanted to learn more about it. In a kind of magical way money showed up in the form of taxreturns. I invested in the best computer I could buy and two months later I landed a job so I could support me and my little son.

From the 8 forms of capital, knowing got me thinking most. What if this form is connected to time? I follow my instinct in what I want to learn. Normally I will need it at some point and then I can do things more efficient and spare me time to do other things. And learning makes me happy, which improves my quality of life.

Hello Helga,

The 8 forms of capital do certainly interrelate! In your example you were able to get financial capital to get material capital in form of the computer, allowing you to increase your knowledge capital that ended up resulting in a job supplying more financial.

Nice observation about knowledge being connected to time as well. I hadn’t considered that before but can certainly see where that happens! In fact today in the studio I’m going to be seeing the reverse of that. My prior lack of knowledge led to an issue I’m now going to be spending more time working to fix. Of course this new knowledge should prevent it from happening again, thus giving me back the time in the future.

Very enjoyable and thought provoking way of looking at this–attending to the gap between income and expenses, the savings. Thank you for this helpful change of focus.

My pleasure Mark. Thanks for the comment. Sometimes just a shift in focus can be a very powerful thing!

Mark, one of the most thought-provoking articles I’ve read recently. I also looked up images of your art and they are stunning. I am retired and financially stable, but actively engaged in staying that way. Thanks for the time you put into this blog.

Thank you Jennifer and congratulations on achieving a financially stable retirement! It’s nice to know people do appreciate the time it takes to do this blog.